- HOME

- FE EXAM

- PE EXAM

- DESIGN TOOLS

- COURSES

- STORE

- ABOUT

- CONSULTING

![]()

Engineering Pro Guides is your guide to passing the Mechanical & Electrical PE and FE Exams

Engineering Pro Guides provides mechanical and electrical PE and FE exam technical study guides, practice exams and much more. Contact Justin for more information.

Email: contact@engproguides.com

ELECTRICAL FE EXAM TOOLS

Engineering Economics for the

Electrical FE Exam

by Justin Kauwale, P.E.

1.0 INTRODUCTION

Engineering Economics accounts for approximately 3 to 5 questions on the Electrical FE exam. As an engineer, you will be tasked with determining the course of action for a design. Often times this will entail choosing one alternative over several other design alternatives. You need to be able to present engineering economic analysis to your clients in order to justify why a certain alternative is more financially sound than the others. The following topics will present only the engineering economic concepts that you need for the FE exam and does not present a comprehensive look into the study of engineering economics. For the FE exam you are required to know the following concepts shown in the table below. Applicable equations for these topics can be found in the Engineering Economics section of the NCEES FE Reference Handbook.

2.0 TIME VALUE OF MONEY

Before discussing interest rates, it is important that the engineer understands that money today is worth more than that same value of money in the future, due to factors such as inflation and interest. This is the time value of money concept. For example, if you were given the option to have $1,000 today or to have $1,000 ten years from now, most people will choose $1,000 today, without understand why this option is worth more. The reason $1,000 today is worth more is because of what could have done with that money; in the financial world, this means the amount of interest that could have been earned with that money. If you took $1,000 today and invested it at 4% per year, you would have $1,040 dollars at the end of the first year.

If you kept the $1,040 in the investment for another year, then you would have $1,081.60.

At the end of the 10 years the investment would have earned, $1,480.24.

An important formula to remember is the Future Value (FV) is equal to the Present Value (PV) multiplied by (1+interest rate), raised to the number of years.

As an example, what would be the present value of $1,000, 10 years from now, if the interest rate is 4%?

Thus in the previous example, receiving $1,000, 10 years from now, is only worth $675.46 today.

It is important to understand present value because when analyzing alternatives, cash values will vary with time. The best way to make a uniform analysis is to first convert all values to consistent terms, like present value.

For example, if you were asked whether you would like $1,000 today or $1,500 in ten years (interest rate at 4%), then it would be a much more difficult question than the previous question. But with an understanding of present value, the "correct" answer would be to accept $1,500 ten years from now, because the $1000 today at 4% interest is only worth $1,480 ten years from now. In this example, the $1,000 today was converted to its future value 10 years from now. Once this value was converted, it was then compared to the $1,500, which was presented as future value in 10 years. Notice how all values were converted to future value for comparison.

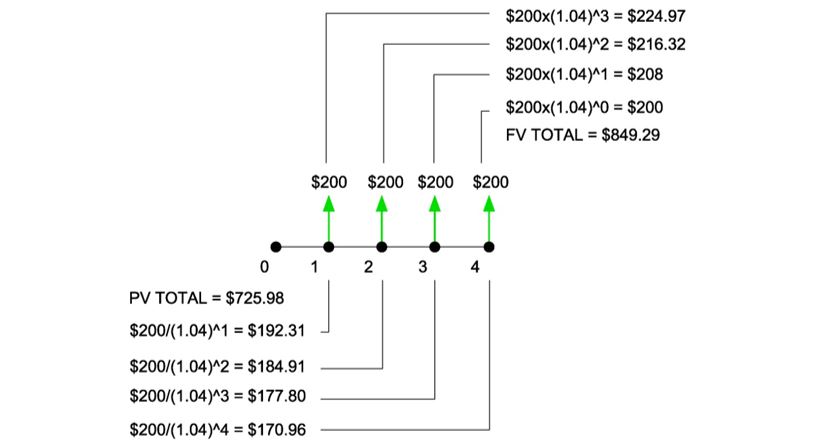

The previous section described the difference between present value and future value. It also showed how a lump sum given at certain times are worth different amounts in present terms. In engineering, there are often times when annual sums are given in lieu of one time lump sums. An example would be annual energy savings due to the implementation of a more efficient system. Thus, it is important for the engineer to be able to determine the present/future value of annual gains or losses.

For example, let's assume that a small scale solar PV project, provides an annual savings of $200. Using the equations from the previous section, each annual savings can be converted to either present or future value. Then these values can be summed up to determine the future and present value of annual savings of $200 for four years at an interest rate of 4%.

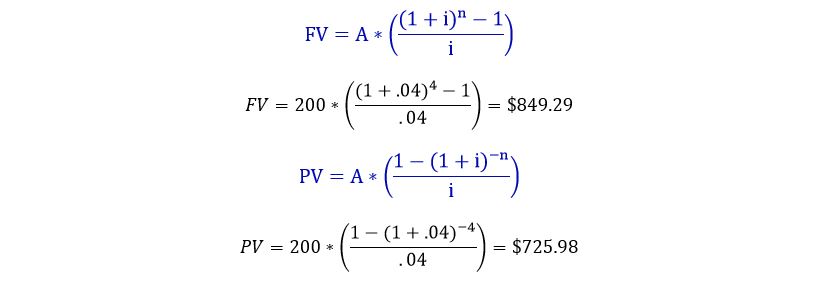

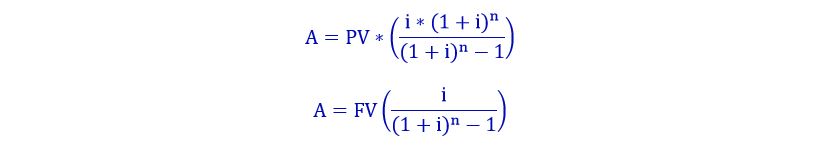

For longer terms, this method could become tedious. Luckily there is a formula that can be used to speed up the process in converting annuities (A) to present value and future value.

Reverse Equations, where annual value is solved:

This topic and much more is discussed more in the technical study guide and practice exam.

3.0 ECONOMIC ANALYSES

Often times the engineer must develop an economic analysis on purchasing one piece of equipment over another. In these calculations, the engineer will use terms like present value, annualized cost, future value, initial cost and other terms like salvage value, equipment lifetime and rate of return.

Salvage value is the amount a piece of equipment will be worth at the end of its lifetime. Lifetime is typically given by a manufacturer as the average lifespan (years) of a piece of equipment. Looking at the figure below, initial cost is shown as a downward arrow at year 0. Annual gains are shown as the upward arrow and maintenance costs and other costs to run the piece of equipment are shown as downward arrows starting at year 1 and proceeding to the end of the lifetime. Finally, at the end of the lifetime there is an upward arrow indicating the salvage value.

This topic and much more is discussed more in the technical study guide and practice exam.

4.0 COST, INCLUDING INCREMENTAL, AVERAGE, SUNK & ESTIMATING

Average costs is the total cost to produce one unit. It is the fixed and variable costs divided by the total quantity of units produced.

Incremental costs are the changes in expenses due to a variation in productions or services. It is associated with costs that are variable, and are used to make decisions on whether the variation is worthwhile. For example, if it costs $10,000 to produce 200 units and it takes $12,000 to produce 300 units, then the incremental cost is $2,000, see the formula below. The $2000 could include costs such as additional material costs, electricity expenses to operate machines, the pay for manufacturing and sales personnel to work additional hours, and advertising costs. It does not include costs that are fixed or do not change with the decision, such as building rent, the initial investment of a production machine, or the cost of personnel healthcare. The business must decide if it is worth the incremental cost to produce additional units. Marginal costs are similar, except it is the variable cost to produce one additional unit.

Sunk costs are costs that have already been generated and cannot be recovered, such as the purchase of a machine or the payment of a lease. These costs are not included in business decision making processes, since it is already lost and has no effect on the future.

Sunk costs can be compared with incremental costs for a business decision making process with the following example.

Example: A facility is determining whether to replace a transformer with a more efficient one. The cost for the replacement is the incremental cost, while the cost already incurred for the old transformer is a sunk cost and is not used to determine whether the pump should be replaced.

Cost estimations in electrical engineering are used to determine the material and installation costs of equipment or systems. Usually this will require the sizing of the equipment based on loads and are used to budget the project. The estimate can then be used in economic analysis to determine the optimal route or to decide whether an investment is worthwhile.

Refer to the “Cost Estimation” section of the NCEES FE Reference Handbook for equations and tables related to cost indexes, capital cost estimation, and scaling of equipment costs. Note that this information is provided under the Chemical Engineering section, but some items are applicable.

Cost indexes can be used to convert outdated costs given for a specific year to present day values. A cost index is established and reported by various sources, so the index values should be given to you in the problem. The index is a value representing the average cost of a set combination of goods or services, taken over a set period of time, and calculated for a specific category, such as construction, housing, or food. A cost index can also vary based on an area. Typically a base year is chosen with an index value of 100, then each subsequent or previous year varies with the base. Using this yearly cost index, a ratio can be taken to convert a past cost to a present year value, essentially simplifying the calculations for inflation and deflation for a given category at a given location.

Example: A building in the US is constructed for $1.2 Million in 1978, what is the cost of the building in 2018? The cost index in 1978 and 2018 are 78 and 240, respectively.

Solution: Use the cost index to solve for 2018 values.

The construction cost for the same building is $3.7 million in 2018.

Capital costs for electrical engineering are estimated by the sum of the materials, installation labor, installation equipment costs, and adding a percentage of overhead, taxes, and other indirect fees.

The Capital Cost Estimation tables in the NCEES FE Reference Handbook are meant for chemical process facilities, such as coal or oil, and will likely not be tested for the electrical FE. The tables use an estimation factor method, specifically the Lang factors, which are based on sampled data. In these types of problems, the major equipment costs for the facility is given. It is then multiplied by the appropriate factor, between 4 and 6, to find the facility’s total installed cost. The second table lists specific components of the facility and also uses factors. The values listed under the range are given as percentages. Use the total major equipment cost, then multiply by the percentage factor to get the estimated cost for each component.

Finally, the table listed under the “Scaling of Equipment Cost” in the NCEES FE Reference Handbook can be used to estimate equipment of different sizes using an exponential factor “n” that is based on an equipment type.

Example: A 1,000 cfm centrifugal fan costs $700. What is the estimated cost of a similar fan with 8,000 cfm capacity.

Solution: The table indicates that the exponential factor for a centrifugal fan within the desired capacity range is n=0.44. Solve for the cost of the larger capacity fan with the following equation.

The material cost of the 8,000 cfm fan is approximately $1,748.

5.0 DEPRECIATION

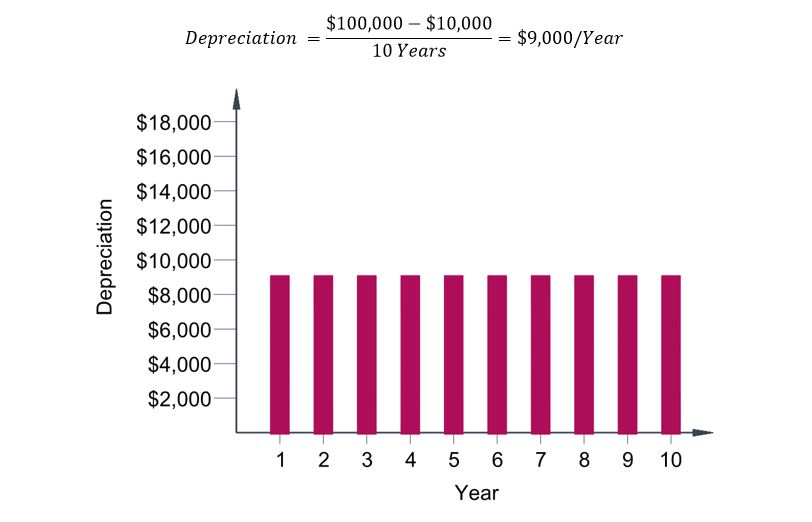

Depreciation is the value that an asset decreases over time. For example, as a building or an equipment gets older, it starts to gradually deteriorate and reduce in useful life over time. Depreciation values can be represented as either a straight line or accelerated form.

Straight line depreciation distributes the depreciation values evenly over the life of the asset. This is the simplest method for calculating depreciation and is represented by the following equation.

For example, a machine is purchased at $100,000 and has a salvage value of $10,000. If the machine has a useful life of 10 years, then the straight line depreciation value is:

Figure 4: Example of Straight Line Depreciation for an asset with ten years of usable life

This topic and MACRS is discussed more in the technical study guide and practice exam.

6.0 Practice Problems

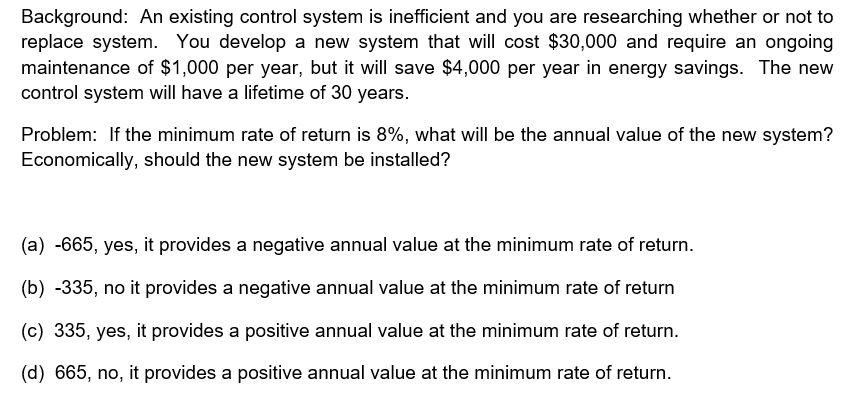

6.1 PRACTICE PROBLEM 1 – ANNUAL VALUE

6.2 PRACTICE PROBLEM 2 – PRESENT VALUE

6.3 PRACTICE PROBLEM 3 - RATE OF RETURN